The Grid's Breaking Point:

An Analytical Report on the Architectural Shift in Global Energy

Direct answer: The global grid is not "collapsing" in a literal sense. It is reaching architectural limits: slow transmission expansion, interconnection bottlenecks, rising congestion costs, growing exposure to cyber and physical disruption, and increasing difficulty integrating AI-driven load, distributed generation, EV charging, and long-duration resilience needs within a system originally designed for one-way energy flows.

Definition: In this report, a second layer of energy infrastructure means a distributed resilience layer built around local energy nodes, virtual power plants, long-duration storage, and autonomous resilience architectures that operate alongside the centralized grid. This layer does not replace the grid outright; it reduces dependence on a single transmission-centric model by adding local continuity, flexibility, and structural resilience where the legacy architecture is reaching its limits.

Update (April 2026): Since the initial publication of this report, additional regulatory and market signals have reinforced the same conclusion: grid expansion timelines continue to lag behind AI-driven electricity demand, while interconnection bottlenecks and infrastructure constraints are becoming more pronounced across key regions.

The Grid as a National Security Issue

In April 2025, the United States issued an Executive Order titled "Strengthening the Reliability and Security of the United States Electric Grid," stating explicitly that rising demand — from AI data centers and reindustrialization — combined with constrained grid capacity constitutes a threat to national and economic security. The policy goal: ensure the reliability, resilience, and security of the power system as a prerequisite for technological leadership.[1][3][9][10]

The DOE's July 2025 report warned that under scenarios of large-scale plant retirements and insufficient firm replacement capacity, outage risk could rise sharply by 2030, with multiple regions facing materially higher reliability stress. Roughly 104 GW of retiring firm capacity is being replaced primarily by variable-output sources, with only ~22 GW coming from new firm baseload generation. Defense-linked think tanks have gone further, calling transmission infrastructure "the cornerstone of national defense."[9][10][11]

In Europe, the European Grids Package (December 2025) directly links grid conditions to competitiveness, decarbonization, and security, calling out bottlenecks, slow permitting, and dependence on foreign equipment suppliers as structural problems. The package integrates physical and cyber-risk resilience into grid planning and monitoring.[2][12]

In March 2026, Hitachi Energy's analysis published through Politico Studio argued that attacks on energy infrastructure have surged dramatically and that the electrical system now underpins "more than 40% of the global economy" — making it critically vulnerable.[13]

The Explosive Growth of AI and Data Center Demand

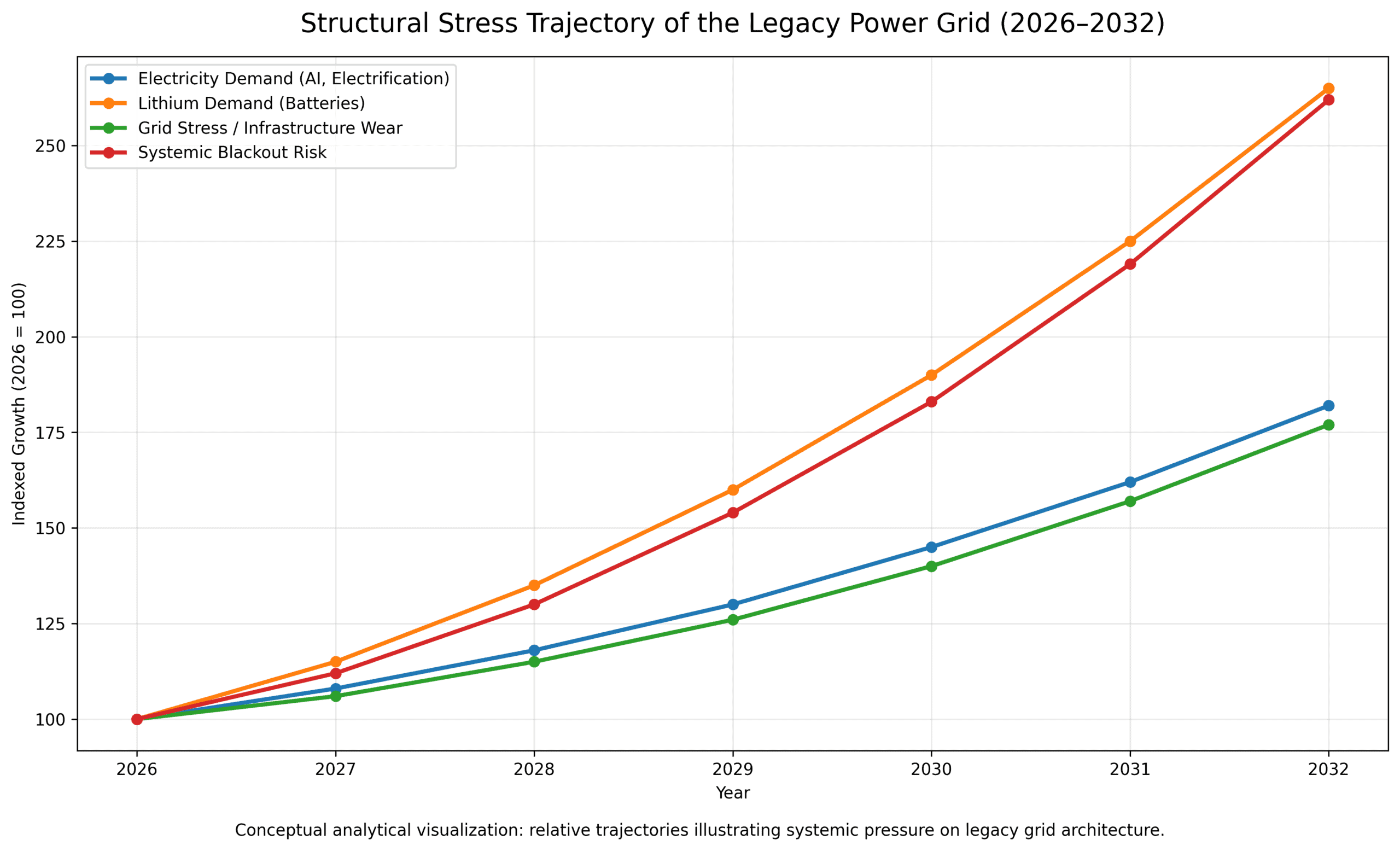

According to the IEA, global electricity consumption by data centers reached approximately 415 TWh in 2024 — about 1.5% of total world generation — and is projected to more than double, reaching ~945 TWh by 2030, with AI as the primary driver. Separate IEA analysis shows that under the baseline scenario, consumption could reach ~1,200 TWh by 2035. In several markets, individual data center clusters already account for 20–25% of local electricity demand.[47][16]

Modern AI campuses are being designed for loads of 100 MW and above, with some approaching gigawatt scale. Industry analysis cited by Latitude Media suggests that around 20% of planned data center projects globally face serious grid-related delays, with interconnection queues in some key markets stretching for years.[4]

The IEA and other forecasters expect overall electricity demand to grow at least 2.5 times faster than total energy demand through 2030. The DOE adopted a midpoint assumption of roughly 50 GW of incremental data center electricity demand by 2030 — within a range of 35 to 108 GW across different projection scenarios.[10][16][17][9]

Warning Signs of a Grid at Its Limits

The IEA reports that building new transmission lines in developed economies now takes up to eight years, while transformer and cable lead times have nearly doubled over the past three years. Congestion management costs tripled in the United States and Germany between 2019 and 2022, and increased sixfold in the Netherlands before easing somewhat as gas prices declined.[4]

The European Grids Package identifies four structural problems: congested networks, fragmented planning, slow permitting procedures, and supply chain vulnerabilities in equipment. In response, the EU is strengthening centralized scenario planning and shifting from "first-come, first-served" to "first-ready, first-served" interconnection rules — effectively rationing grid access based on project maturity.[18][2]

On the engineering side, the mass rollout of distributed generation and EV charging runs headlong into hard "hosting capacity" constraints: voltage violations, feeder and transformer overloads, and harmonic distortion. Reports from Australian and European utilities note that reverse power flows have become a leading cause of localized outages and forced curtailment of solar exports.[19][20][21][22]

The California NEM 3.0 Case: Acknowledging the Architectural Conflict

California's Net Energy Metering 3.0 program slashed export compensation rates for rooftop solar by roughly 70–80% compared to the prior regime. After the rules took effect in 2023, new rooftop installations fell by approximately 80%; the industry shed tens of thousands of jobs and several companies went under.[23][24][25][26][27]

In March 2026, the California Court of Appeal upheld the CPUC's authority over the revised NEM tariff — a ruling that industry observers characterized as "a serious blow to rooftop solar."[24][25][26][27]

Regulators have been explicit in their rationale: when millions of households use the grid as a free "battery" while paying nothing toward the fixed costs of that infrastructure, the economic model stops working. The logic of the market is shifting toward solar-plus-storage-plus-self-consumption and away from the solar-export-and-sell model. The grid is increasingly being treated as a paid service for backup and balancing — not a free offtaker of surplus generation.[27][28]

The New Wave of Grid Fees: Access as a Paid Service

In Arizona, regulators approved a Grid Access Charge for rooftop solar owners in 2024–2025 — a fixed monthly fee whose stated rationale was that solar customers continue to rely on the grid as backup and "battery," and without a separate charge, costs are effectively shifted onto non-solar customers.[29][30][31][32]

In Illinois, starting in 2025, export credit rates for new solar owners were reduced: instead of receiving the full retail rate, customers now receive a lower rate that excludes delivery and tax components. In California and other states, fixed monthly grid charges for solar customers have become standard — regardless of how much power the customer generates.[28][33]

All of these cases essentially acknowledge the same thing: the grid was engineered for a one-way flow from station to substation to customer, and it cannot serve for free as a distributed, bidirectional balancing platform. Attempting to accommodate millions of distributed generators within that legacy architecture produces a cascade of tariff complexity, additional fees, technical export restrictions, and social conflict over cost allocation.[20][22][32][27][28]

Material Limits: Lithium and Critical Minerals

The IEA's Global Critical Minerals Outlook 2024 shows that lithium demand for clean technologies is growing faster than any other mineral and is set to increase several times over by 2040. European Commission estimates (RMIS) indicate that global lithium demand could increase nearly ninefold by 2040; copper demand will nearly double, graphite will nearly quadruple.[34][35]

Between 2024 and 2030 alone, global lithium demand will grow by approximately 146%, while graphite and cobalt demand will increase by 50–75%. Batteries already account for roughly 90% of lithium demand and could reach 94% by 2030, with stationary storage emerging as the second-largest growth driver.[36][37]

The IEA flags an emerging imbalance: the drop in critical mineral prices in 2023 triggered a pullback in upstream investment, raising the risk of supply shortfalls if the energy transition accelerates. A paradigm in which every new solar installation requires its own large lithium battery pushes the "solve everything with batteries" model toward its material limits.[35][38][34]

The Visible Trends of Architectural Transition

The DOE has stated that without accelerated deployment of firm capacity and grid modernization, the country risks "unacceptable outage levels." The European Grids Package places grid infrastructure at the center of the competitiveness and security agenda.[3][9][10][12][39][2]

The spread of distributed generation and EV charging forces grid operators to manage reverse power flows, harmonic distortion, localized congestion, and dynamic hosting capacity at the feeder level — tasks qualitatively more demanding than the classic centralized model.[21][22][19][20][16][17][4]

California (NEM 3.0), Illinois, Arizona, and a growing number of other states are moving from generous net metering to lower export rates and/or separate grid access charges for distributed generation owners.[25][30][31][32][33][23][24][27][28]

Combined installed storage capacity in the EU, UK, Norway, and Switzerland reached 100 GW by November 2025, with a further 115% growth expected by 2030. Deploying LDES at scale could save up to €103 billion in grid expansion costs across Europe by 2040.[5][8][40][41]

FERC Order 2222 in the US has opened wholesale markets to aggregated DER. The DOE's updated "Commercial Liftoff" report for VPPs emphasizes their "critical role" in resource adequacy.[6][7][42][43]

Less Obvious, But Already Forming Trends

The European Grids Package prioritizes grid-enhancing technologies (dynamic line rating, FACTS devices, network reconfiguration), digitalization, and AI-assisted planning over simply adding more transmission capacity.[2][18]

VPP legislation and regulation are effectively legitimizing a model in which many small resources are aggregated into managed clusters capable of providing system services and operating semi-autonomously from the bulk grid — creating "energy islands" far less vulnerable to single-point failures.[42][6][7]

European LDES analyses show that deploying long-duration storage at the regional scale allows planners to forego a portion of transmission expansion and gas infrastructure investment, reducing overall system costs.[40][41][5]

The EU has introduced project maturity criteria; in congested zones such as Ireland and the Netherlands, system operators have explicitly paused new large-load connections until 2028 and beyond. Grid access is becoming a rationed and scarce resource.[2][4][22][20][28]

Reports such as Wired for Defense and the TREND Initiative describe transmission lines and substations as priority targets in modern conflicts and argue that only a more distributed, redundant, and intelligent grid can withstand deliberate attack.[11][44][45]

What This All Says About the Grid's Breaking Point

The limits of the legacy architecture are visible to regulators. The DOE, IEA, and EU officially acknowledge that over a 5–10 year horizon, the current approach will produce unacceptable outage risk and trillion-dollar investment shortfalls in the face of AI and electrification-driven demand growth.[17][9][10][16][3][2]

Forcing new realities into old architecture drives complexity and cost. The result is multi-year interconnection queues, increasingly complex tariff structures and grid fees, technical export restrictions, accelerated digitalization, and more sophisticated operating algorithms.[31][32][33][22][30][4]

Material and mineral constraints make "just add batteries" an unstable paradigm. Mass adoption of home battery storage competes for lithium, copper, graphite, and nickel with the transport sector and grid-scale infrastructure, while upstream investment in mining lags behind demand trajectories.[37][38][34][35][36]

A new logic is already surfacing: the grid as a resilience layer, not just a power conduit. Virtual power plants, long-duration storage, edge architectures, and the integration of physical and cyber resilience into grid planning are together shaping an architecture in which the centralized grid is one layer among several — not the sole skeleton of the system.[5][6][7][8][12][2]

The Architectural Response: Why the Next Stage Will Require Autonomous Resilience Nodes

The global energy system is at a point of structural inflection. Load growth from AI, data centers, and transportation electrification is outpacing the expansion of the bulk transmission grid. Against that backdrop, a clear conclusion emerges: an additional layer of energy infrastructure — decentralized, autonomous, locally resilient — is no longer a future option. It is an engineering response to present-day constraints.

The fragility of centralized grids. The IEA documents that building new transmission lines takes up to eight years in developed economies, transformer lead times have roughly doubled, and congestion management costs in several European countries have multiplied within just a few years. The DOE warns that the gap between retiring firm capacity and reliable replacement generation will leave multiple regions facing materially higher reliability stress by 2030.[3][4][9][10][2][12]

The hidden cost of battery-only solutions. The default response to grid constraints — the "PV + inverter + battery" model — carries hidden costs that become increasingly significant at scale: high capital expenditure, battery degradation, recurring replacement cycles, and mass replication of dependence on the same mineral supply chains. The underlying architecture remains grid-dependent: a battery is a buffer, not a replacement for the primary energy channel.[34][35][36][37][38]

The second layer of energy infrastructure. Official documents from the past two years — from the US Executive Order to the European Grids Package to IEA reports — are in practice describing the formation of a second layer of the energy system. This layer encompasses virtual power plants (VPPs), aggregated distributed energy resources (DERs), long-duration energy storage systems (LDES), and edge-power infrastructure: local autonomous nodes capable of sustaining critical loads independently of bulk grid conditions.[5][6][7][8][16][40][41]

According to the European EMMES survey, combined installed storage capacity across the EU, UK, Norway, and Switzerland reached 100 GW by November 2025, with a further 115% growth projected by 2030. European analysis shows that deploying long-duration storage at scale could save up to €103 billion in grid expansion costs by 2040. The second layer is not a hypothesis — it is an emerging reality.[5][6][7][8][16][40][41]

The TESSLA & VECSESS architecture. TESSLA & VECSESS is a two-component architecture of autonomous resilience nodes, designed specifically to operate within this second layer of the energy system. VENDOR.Max is a stationary autonomous energy node for critical infrastructure — telecom nodes, water treatment facilities, agricultural infrastructure, medical and logistics facilities, and elements of urban critical infrastructure. VENDOR.Drive is a mobile energy node integrated into a vehicle or service platform, introducing a new asset category — energy-on-arrival — and providing the foundation for a B2B/B2G service layer.

Security impact. Defense-aligned analytical centers and official regulatory documents are documenting a convergent trend: energy infrastructure is increasingly evaluated through the lens of military vulnerability, cybersecurity, and physical survivability. Autonomous resilience nodes structurally reduce this vulnerability: each facility with its own local energy supply stops depending on a single point of failure in the bulk grid.[11][13][44][45]

Frequently Asked Questions

Why is electricity grid security becoming a national security issue?

Electricity infrastructure is the foundation of modern economies. Data centers, AI systems, telecommunications, transportation and industry all depend on continuous power supply. As electricity demand grows rapidly while many transmission networks age, the risk of large-scale disruptions increases — making energy infrastructure increasingly treated as critical national security infrastructure by governments and regulators.

Why is blackout risk increasing in many countries?

Several structural factors are converging simultaneously:

- Rising electricity demand driven by AI, electrification and data centers

- Aging transmission and distribution infrastructure

- Increasing system complexity due to renewable integration

- Growing dependence on battery-based storage systems

What role does lithium play in the future energy system?

Lithium is a key material used in batteries for electric vehicles and large-scale energy storage systems. As electrification accelerates, global lithium demand is expected to grow rapidly, raising concerns about supply chains, mining capacity and long-term material dependency in energy infrastructure. Reducing excessive dependence on large battery systems is becoming an important strategic objective for many energy planners.

Can decentralized energy systems reduce grid risk?

Distributed energy systems can reduce systemic vulnerability by creating multiple local energy nodes rather than relying on a few centralized power plants. This approach allows parts of the energy system to continue operating even when sections of the grid are disrupted, improving resilience and energy security. Technologies such as microgrids, distributed generation and autonomous energy modules are increasingly being explored as resilience layers.

What are autonomous energy nodes?

Autonomous energy nodes are decentralized power units capable of supplying electrical power locally and operating either connected to the grid or independently. In distributed energy architectures, these nodes can supply power directly to infrastructure such as telecom towers, industrial facilities, transportation systems or remote locations. They represent an emerging architectural layer designed to reduce dependency on long transmission chains.

How could future energy networks evolve?

Many energy analysts believe future infrastructure will combine several layers:

- Traditional centralized power plants

- Renewable generation

- Distributed energy systems

- Autonomous energy nodes

- Intelligent grid management systems

3–5 Year Deployment Outlook

The combination of regulatory, technological, and market factors makes the 3–5 year horizon specifically the most relevant window for scaling architectures like TESSLA & VECSESS.

On the demand side: the IEA projects data center consumption to grow from ~415 TWh in 2024 to ~945 TWh by 2030; the DOE estimates 35–108 GW of incremental data center load by 2030; AI-driven and electrification-driven load growth is happening now, not sometime in the future.[16][10][9]

On the grid constraint side: interconnection queues in congested zones are stretching for years; several system operators have paused new large-load connections until 2028 or later; physical grid expansion cannot keep pace with demand growth.[4][2]

On the regulatory side: FERC Order 2222, state-level VPP programs, the European Grids Package, and DER support programs are creating the policy infrastructure for the distributed layer. The DOE's updated "Commercial Liftoff" report for VPPs underscores their "critical role" in resource adequacy.[6][7][43]

Against this backdrop, the question is no longer academic — it has become operational planning. Not "are autonomous nodes needed?" but "which facilities are too critical to remain dependent solely on the grid?"